REPORT ON CORPORATE GOVERNANCE

Annual Report 2015

Karin Technology Holdings Limited

33

The ARMC and Board are satisfied that the appointment of different auditors for its subsidiaries incorporated in Singapore

and the People’s Republic of China (“

PRC

”) would not compromise the standard and effectiveness of the audit of the

Company. The Company therefore is in compliance with Rules 715 and 716 of the Listing Manual of SGX-ST. The

Company has engaged suitable auditing firms for its significant foreign-incorporated subsidiaries and associated company.

Accordingly, the names of auditing firms for its significant subsidiaries and associated companies are disclosed below,

pursuant to Rule 717 of the Listing Manual of SGX-ST:

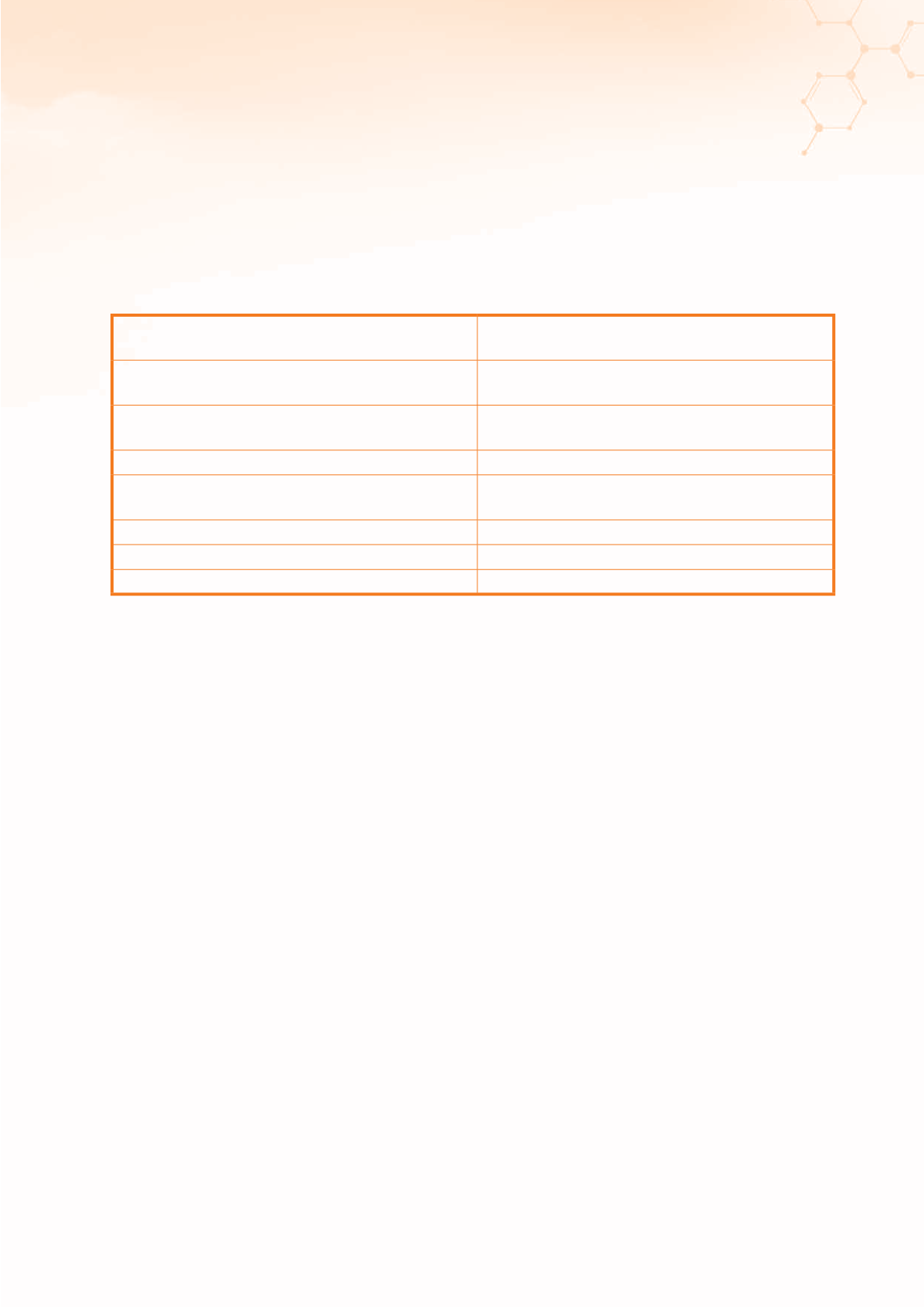

Name of significant subsidiaries and associated

companies

Name of auditing firm

New Spirit Electronic Technology Development

(Shenzhen) Company Limited

Wongga Partners Certified Public Accountants

(SZ) General Partner

Karin Electronic Trading (Shenzhen) Company Limited Wongga Partners Certified Public Accountants

(SZ) General Partner

Karin International Trading (Shanghai) Company Limited Shanghai JiaLiang CPAs

Karltec Information System (Shenzhen) Company Limited Wongga Partners Certified Public Accountants

(SZ) General Partner

Matrix Power Technology (Shenzhen) Co. Ltd.

Shenzhen Leinuo Certified Public Accountants

I M I Kabel Pte. Ltd.

KBH Integra PAC

Shanghai Cosel International Trading Co. Ltd.

Shanghai Xin Zheng Guang Certified Public Accountants

The ARMC meets periodically and also holds informal meetings and discussion with Management from time to time.

The ARMC has full discretion to invite any director or executive officer to attend its meetings.

The ARMC met, including but not limited to telephone conference, with the external auditors without the Company’s

Management, at least once annually.

The ARMC had established a written whistle-blowing policy, by which staff of the Company and any other persons may,

in confidence, raise concerns about possible improprieties in matters of financial reporting or other matters. Whistle-

blower channels, such as email addresses and phone numbers are created for reporting of whistle-blowing events. All

staff should be aware about the existence of the whistle-blowing policy. The whistle-blowing policy has been posted on

the Group’s corporate website. Each of the ARMC member or two of the senior management is the channel for reporting

of suspicious non-compliance or improprieties. The ARMC obtained quarterly update on the status of whistle-blowing.

The ARMC has reasonable resources to enable it to discharge its functions properly. The ARMC is updated annually on

any changes in accounting standards by the external auditors. No former partner or director of the Company’s existing

auditing firm is a member of the ARMC.

PRINCIPLE 13 – INTERNAL AUDIT

The Company has established an Internal Audit Department and employed a full time Internal Auditor (“

IA

”) to perform

the internal audit function and to improve the system and processes of internal controls of the Company. IA primarily

reports to the Chairman of ARMC.

The ARMC has bi-annually reviewed the internal audit programme, the scope and results of internal audit procedures.

The ARMC reviews the adequacy and effectiveness of the internal audit function. The ARMC is satisfied that the internal

audit function is adequately resourced and has appropriate standing within the Company. The ARMC is also satisfied

that the IA is staffed by suitably qualified and experienced personnel.